We usually think about oil, specifically fuel for road vehicles, when the spectre of energy shortages is raised. Today, our supply of natural gas is more vulnerable to early price increases. In energy terms, Ontario uses about as much natural gas as oil (see Figure 1), but the use of natural gas is spread across more sectors (see Table 1) and may for that reason be less conspicuous.

It's easy to take comfort in a recent report by the U.S. Energy Information Administration that points to a bountiful supply of natural gas worldwide.15 Another such report is that of the International Energy Agency, which said that "Reserves of coal and natural gas are particularly abundant, while there is no lack of uranium for nuclear power production."16

Close reading of these reports reveals that markets for natural gas are essentially continental. It is difficult to move natural gas across oceans. It can be liquefied, shipped as liquefied natural gas (LPG), and "regassed," but this process is energy-consuming, expensive, and potentially dangerous. (Indeed, one of the reports suggests that the NIMBY challenges in siting a further LPG-receiving terminal in the U.S. may be "insurmountable.")17

At present, the U.S. and Canada are responsible for about 35% of natural gas consumption worldwide but have only about 4% of reserves. (Mexico is a net natural gas importer--from the U.S.--and is likely to remain so.) Moreover, North American demand, i.e., potential consumption, is set to grow by 50% by 2020, largely because of expansion of natural-gas-fuelled electricity generation in the U.S. Much of the increase in natural gas supply is projected to come from Canada, which currently uses more than half its production to provide for about 20% of U.S. consumption in an integrated market. LPG imports from outside North America are not expected to provide more than a few percent of 2020 demand.18

The problem with the above demand projection is that there seems to be little potential for increasing North American natural gas production. The Canadian situation has been charted by the Alberta Energy and Utilities Board. It envisages production there gradually declining after 2003.19 The Canadian Gas Potential Committee--a group of senior geoscientists from industry and government--has noted that supplies from the Scotia Shelf and Mackenzie Delta together could not amount to more than about 15% of present production.20 The Committee's report concluded that "the era of low-cost gas supplies has now effectively ended."

The situation in the U.S. is, if anything, bleaker. It was set out in testimony to the U.S. Congress in July 2002 by Matthew Simmons, a banker specializing in energy investments and a member of the U.S. National Petroleum Council, an oil and natural gas advisory committee to the Secretary of Energy. Mr. Simmons said that natural gas supply "continues to stay flat in the U.S. as it has done for the past eight years, despite a natural gas drilling boom of historic proportion in both the U.S. and Canada. ... The precarious supply/demand imbalance of 15 months ago is now headed towards a colossal mismatch between a need for demand to soar while supply drops."21

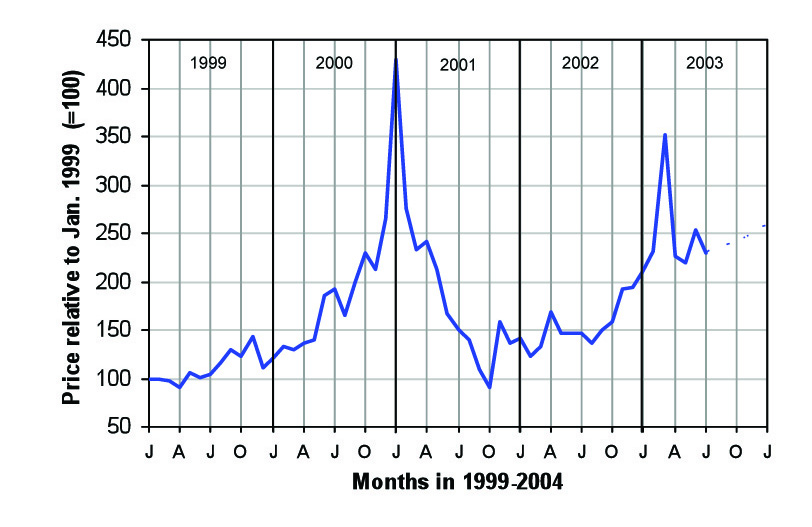

Figure 7. Monthly wholesale natural gas prices

The "imbalance of 15 months ago" referred to a time when natural gas prices in North America reached historic high real values. This peak is shown in Figure 7, which charts wholesale prices for the period January 1999 to July 2003, with anticipated prices to January 2004.22 The imbalance resulted in a more than threefold increase in wholesale prices in January 2001 over the previous year. The period of extreme prices was short-lived but the general result was a 50%-plus increase natural gas bills in the 2000-2001 season in the Central Ontario Zone compared with a year earlier.

Prices returned to quite low levels during the winter of 2001-200223 before entering what may be the beginning of the "colossal mismatch" anticipated by Mr. Simmons. Figure 7 shows a further price peak during the winter of 2002-2003, without the subsequent decline to relatively low levels. The likely impact on next winter's retail prices in the Central Ontario Zone is hard to predict. A reasonable guess may be that they will rise to above $0.40 per cubic metre, i.e., to more than 50% above prices at the start of the winter of 2002-2003, and they continue to rise.

It's the longer term that may be the real problem. The Canadian Gas Potential Committee anticipates declines in production of more than 50% by 2020.24 Given the potential demand for natural gas--including plans to convert Ontario's coal-fired generating plants--the discrepancies between North America supply and North American demand will be huge. Real retail prices of natural gas could increase by a factor of several times, enough to cause changes in how and where we live and work.